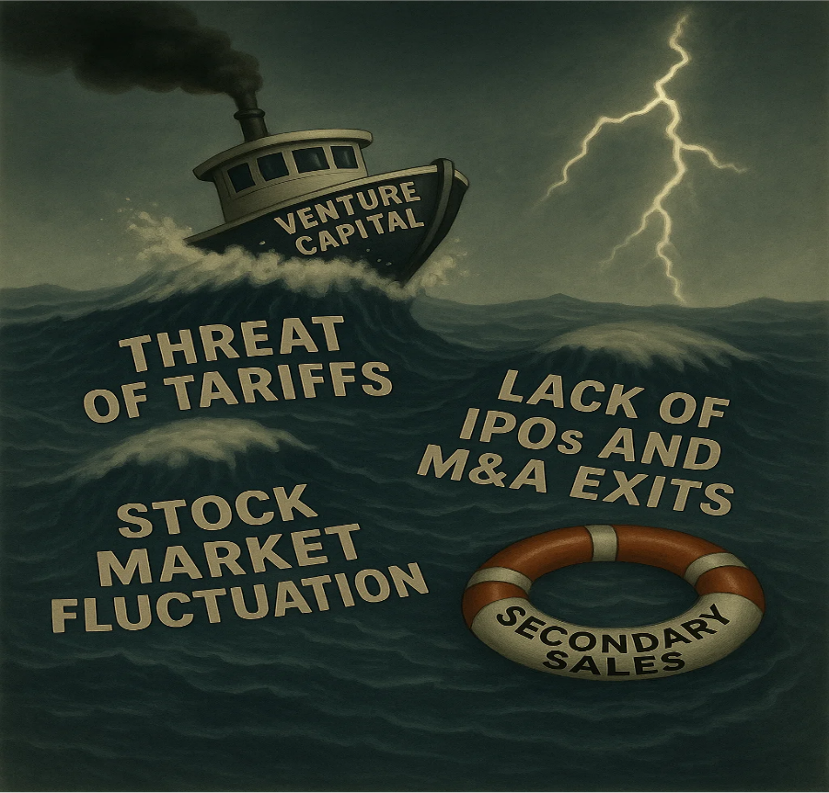

Over the past few weeks, markets have been thrown into chaos with the economic uncertainty surrounding President Trump’s recent tariff policy announcements. The S&P 500 has retreated ~10% off its all-time high in late February, with the VIX more than doubling over that same period. Torsten Slok, chief economist at Apollo Global Management, recently wrote that there is a 90% probability the US will fall into a “Voluntary Trade Reset Recession” if tariff policies remain unchanged1. While the risk of recession will hurt all companies across the board, certain industries will be the hardest hit including:

•Automotive – automakers rely on global supply chains with the majority of parts coming from China, Mexico, Canada and Europe

•Manufacturing and Industrials – imported steel, aluminum and other raw materials will significantly raise input costs

•Computer and electronics – smartphones, semiconductors, laptops, networking equipment are largely sourced from Asia, with a material dependence on China

•Consumer – food, apparel and other retail goods rely heavily on global supply chains. Tariffs will drive up input costs, increasing inflation and reducing household purchasing power

Saints Capital believes that this disruption and market volatility will lead to a generational opportunity for its investment strategy.

Saints is highly optimistic about the buying opportunity we are experiencing in the venture secondary market. Warren Buffett once said that “it’s wise for investors to be fearful when others are greedy and to be greedy only when others are fearful”.2 While it’s impossible to ignore the macro-economic slowdown, what Saints is seeing at the micro-level is that GPs, LPs and founders remain starved for liquidity, which provides for a target-rich environment for their investment strategy. Saints’ pipeline for new GP-led secondary transactions is the most robust we have seen in its 25-year history and believe that the aggressive tariff policies will further catalyze a structural shift in the industry that will provide tailwinds for secondary investors for years to come.

Liquidity Drought Expected to Continue

•With so many scaled, high-growth tech businesses on file to go public at the start of 2025, there was consensus optimism that the 3-year drought in venture liquidity would come to an end. Clearing this backlog would have undoubtedly given GPs and LPs some reprieve, but the illiquidity issues in venture have become more structural than temporal in nature.

•Saints estimates that there is already $225 billion of NAV locked up in venture and growth funds that are over 10 years old, and with the significant increase in capital raised from 2016-2021, this number will increase materially in the coming years.3

•The traditional liquidity mechanisms of IPOs and M&A can no longer be relied upon for venture investors. Secondary funds are the market makers for private tech assets and the current market volatility and multiple contraction in the public markets is creating a highly attractive dynamic to thoughtfully invest through this market cycle. The average revenue multiple for public software companies now sits at 4x NTM revenue, which is 30% less than the median average since 2017.4 Only a small percentage of tech companies like Stripe, Klarna, Databricks, Chime, etc. may be able to go public in this market, leaving a nearly endless opportunity for Saints to acquire stakes in solid businesses at significant discounts to the currently depressed public multiples.

Mindset Shift for GPs

•Over the past 5-10 years, Saints has witnessed an accelerated mindset shift from early-stage venture investors to become more proactive on exiting their portfolio. Founders and investors selling shares to secondary investors were once seen as sacrilegious. Over the next 5-10 years, Saints believes this practice will not only be commonplace but encouraged for proper risk and liquidity management.

•The average investment period for an early-stage investor used to be 7-10 years. The steep rise in late-stage capital has enabled founders to keep their companies private longer, which has increased the holding period for early-stage investors to 12-15 years. This structural shift has put significant pressure on the underwriting models for many LPs, who manage both IRR thresholds and cash distributions so that they can re-balance their asset allocations over time.

•While there is much enthusiasm in the venture capital industry over the AI platform shift that is occurring, unless GPs can unlock liquidity to recycle into these new opportunities by raising new funds, capital will remain stagnant in older funds that don’t have exposure to AI startups.

•As such, there is a massive supply and demand imbalance in the venture secondary market today, where the demand for liquidity far outweighs the capital raised in secondary funds focused on the asset class.

In summary, while the daily headlines can be unnerving, Saints’ 25-year track record of investing across boom-and-bust cycles gives them an incredible amount of optimism that the next few vintages of secondary investments will generate highly attractive returns for investors. Saints often says that the only competition they face is the option for GPs to do nothing and wait out the market malaise. However, the venture market has now been in a holding pattern for the past three years and the chorus of LPs wanting liquidity is becoming undeniable. Saints continues to see GPs wanting to execute transactions and is highly optimistic about the quality of opportunities in the pipeline.

Sources

1Apollo Global Management, “How are US consumers and firms responding to tariffs?” by Torsten Slok, Rajvi Shah, and Shruti Galwankar.

2Berkshire Hathaway, “Chairman’s Letter – 1986,” https://www.berkshirehathaway.com/letters/1986.html).

3Pitchbook as of 2Q 2024.

4Pitchbook as of April 9, 2025.

Disclosures & Legal Disclaimer

The information set forth above shall not constitute an offer, solicitation or recommendation to sell or an offer to purchase any securities, investment products or investment advisory services. Offerings are made only pursuant to a private offering memorandum containing important information regarding risk factors, performance and other material aspects of the applicable offering; the information contained herein should not be used or relied upon in connection with the purchase or sale or any security. The information provided herein does not constitute a representation that any investment strategy or fund investment is suitable or appropriate for any person. Discussion of Saints’ investment strategy includes certain target allocations and objectives, which are targets and objectives only, and there can be no assurance that such target allocations or objectives will ultimately be achieved. These materials are confidential and have been prepared solely for the information of the intended recipient and may not be reproduced, distributed or used for any other purposes. Reproduction or distribution of these materials may constitute a violation of federal or state securities laws.